If you are buying or selling a home, you have probably heard the words “deed” and “title” used during conversations with your agent, lender, or attorney. A lot of people assume they mean the same thing. They do not. Understanding the difference between deed and title is one of those foundational pieces of knowledge that can save you from confusion, delays, and potentially expensive mistakes at the closing table. If you are a Michigan home buyer getting started on this journey, this is one of the first things you should get clear on.

As a licensed Michigan Realtor, I see this mix-up constantly. Buyers walk into closings thinking the deed is the title. Sellers sign documents without fully understanding what rights they are transferring. And first-time buyers especially tend to glaze over when these terms come up because nobody has taken the time to break it down in plain English.

So let me do that for you right now. You will understand the difference between a house title vs deed, who holds the title to your home when you have a mortgage, how to get a copy of your property deed, and how all three of these concepts connect to your mortgage.

House Title vs Deed: The Quick Answer

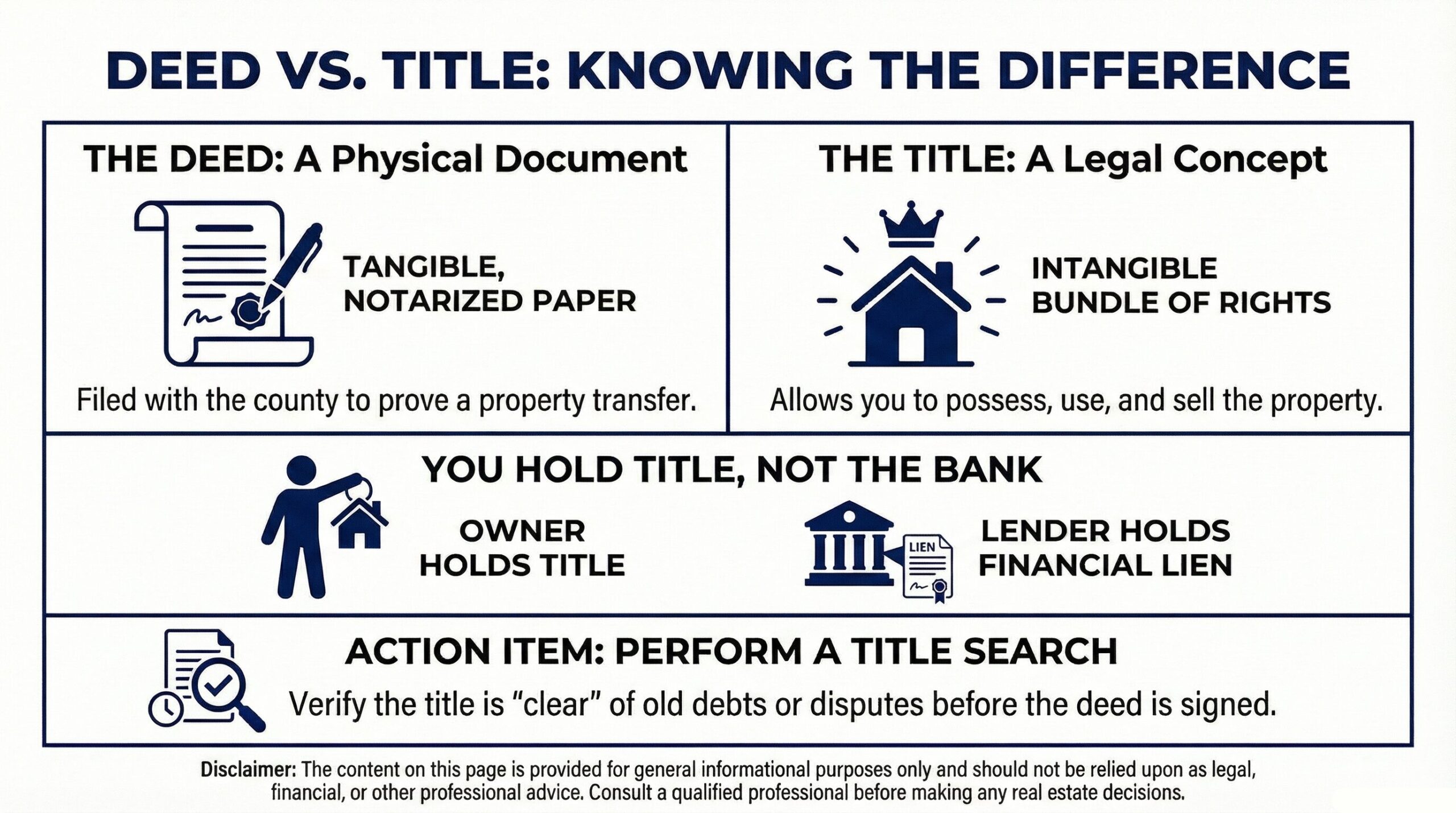

Here is the simplest way to think about it. A deed is a document. A title is a concept.

A deed is the physical, legal document that transfers property ownership from one person (the seller, also called the grantor) to another person (the buyer, also called the grantee). You can hold a deed in your hand, file it in a folder, and store it in a safe.

A title, on the other hand, is the legal right of ownership itself. You cannot physically touch a title. It represents the bundle of rights that come with owning property, including the right to live in it, sell it, lease it, or pass it on to someone else.

Think of it this way. You can walk into a bookstore and pick up a physical book. That book has a title printed on the cover. You can hold the book, but you cannot hold the title separately from the book. In real estate, the deed is the book, and the title is the concept printed on it. One is tangible. The other is not.

What Is a Property Deed?

A property deed is the legal document used in a real estate transaction to transfer ownership from the seller to the buyer. Without a signed and recorded deed, there is no official record that the property has changed hands.

A valid deed typically includes the names of the grantor and grantee, a legal description of the property (including boundaries and property lines), the consideration (usually the purchase price), and the signatures of both parties. The deed is also notarized, which verifies the identity of the person signing it.

Once the deed is signed at closing, it gets recorded with the local county government. That recording is what makes the transfer of ownership part of the public record. This is why you will hear your real estate agent or attorney stress the importance of properly recording the deed. If it is not recorded, disputes about ownership can pop up later.

Types of Deeds You Should Know About

General Warranty Deed. This is the most common type of deed used in traditional home sales. It gives the buyer the strongest level of protection because the seller guarantees that they hold a clear title, that the property is free of liens or encumbrances, and that no one else has a competing claim to ownership. If you are buying a home through a standard purchase, this is likely the type of deed you will receive. All licensed Realtors who are members of the National Association of Realtors are bound by a code of ethics that requires honest representation during these transactions.

Special Warranty Deed. This type is more common in commercial real estate. The seller only guarantees that no title issues arose during the time they personally owned the property. It does not cover problems that may have existed before they took ownership.

Quitclaim Deed. A quitclaim deed transfers whatever ownership interest the grantor has without making any guarantees about the condition of the title. This is typically used when property passes between family members, like a parent transferring a home to an adult child, or between spouses during a divorce. There is no warranty that the title is clear, so it carries the least protection for the buyer.

Deed in Lieu of Foreclosure. This is an arrangement where a homeowner voluntarily transfers the property to their lender to avoid going through the foreclosure process. In exchange, the lender usually agrees to cancel the remaining mortgage balance.

Bargain and Sale Deed. This type falls somewhere between a quitclaim deed and a warranty deed. The seller implies they own the property but does not guarantee the title is free of issues. You will sometimes see this in foreclosure auctions, tax sales, or estate sales where the seller is not willing to take on liability for the title history.

What Is a Title in Real Estate?

While a deed is something you can physically hold, a title is the legal concept of ownership itself. When someone says you “hold title” to a property, they mean you have the legal right to own, occupy, use, and sell that property.

Holding title to a property comes with a specific set of rights. These generally include the right of possession (you can live in and occupy the property), the right of control (you can make improvements or changes), the right of exclusion (you can decide who enters the property), the right of enjoyment (you can use the property as you see fit, within the law), and the right of disposition (you can sell, lease, or transfer the property).

It is worth noting that title also includes any encumbrances attached to the property. This could be a mortgage lien, a tax lien, an easement, or another legal claim. That is why clearing the title before a sale is so important.

Common Ways to Hold Title

Sole Ownership. One person holds full title to the property. They can sell, lease, or bequeath the property without consulting anyone else.

Joint Tenancy. Two or more people hold equal shares of the title. If one owner passes away, their share automatically transfers to the surviving owner(s). This is common among married couples.

Tenancy in Common. Two or more people hold title, but each owns a specific percentage. Unlike joint tenancy, each owner can sell or transfer their share independently without the other owner’s permission.

Who Holds the Title to My Home?

This is one of the most common questions I get from buyers, especially those who are financing their purchase with a mortgage. The short answer is: you do.

If your name is on the recorded deed, you hold the title to the property. That is true even if you have a mortgage. A lot of people assume the bank owns the home until the loan is paid off, but that is not how it works.

When you take out a mortgage, the lender places a lien on the property. A lien is a financial claim, not an ownership claim. It gives the lender the right to foreclose if you stop making payments, but it does not make them the owner. You are the titleholder from the moment the deed is recorded in your name.

Once you pay off the mortgage in full, the lender releases the lien, and you hold the title free and clear with no financial claims attached to it.

Title vs Deed vs Mortgage: How All Three Connect

These three terms show up together constantly during the home buying process, and they each play a different role.

The title is your legal right to own the property. It is the concept of ownership itself.

The deed is the legal document that transfers that ownership from the seller to you. It is the physical proof that a transaction took place.

The mortgage is a loan agreement between you and a lender. The property serves as collateral for the loan. The lender files a lien against the title, which stays in place until the loan is fully repaid.

Here is a real world example of how they work together. You find a home you want to buy. You get approved for a mortgage. At closing, the seller signs the deed, transferring the title to you. At the same time, the lender records a mortgage lien against the property. You are now the legal owner (you hold title), you have the deed to prove it, and the mortgage lien sits on the title until the loan is satisfied. All three exist at the same time, doing different jobs.

Which Is More Important: Title or Deed?

I get asked this question a lot, and the honest answer is that neither one is more important than the other. They are two sides of the same coin.

The deed is the tool that moves ownership from one person to another. Without a deed, there is no official record of the transfer. But without a clear title, the deed itself could be worthless. If the title has issues, such as an unpaid lien or an unresolved ownership dispute, the deed does not make those problems disappear.

Think of it this way. A deed without a clear title is like a receipt for something you cannot actually use. And a title without a deed means there is no documented proof of how ownership was transferred to you.

Both need to be in order for you to have secure ownership of a property. That is why the title search and title insurance steps during closing are so critical. They make sure the deed you are receiving actually delivers clean, undisputed ownership.

How to Get a Copy of Your Property Deed Online (Free or Low Cost)

Whether you just closed on a home or you have owned your property for years, you might need a copy of your deed at some point. Maybe you are refinancing, maybe you need it for estate planning, or maybe you just want to have it on file.

The good news is that most counties make it fairly simple to find your recorded deed. Here is how to get a copy of your property deed online:

Step 1. Visit your county’s Register of Deeds website. In Michigan, each county has its own Register of Deeds office. For example, the Oakland County Register of Deeds has an online search portal where you can look up recorded documents. Wayne County and Macomb County offer similar tools.

Step 2. Search by your name or the property address. Most systems allow you to search by grantor/grantee name, property address, or document number.

Step 3. View or download the deed. Some counties let you view the document online for free. Others charge a small fee (usually a few dollars) to download or print a copy. If you need a certified copy for legal purposes, you may need to request it in person or by mail, and the fee is typically a bit higher.

If you are looking for how to get a copy of your house title specifically, keep in mind that a “title” is not a document you can download. The deed is the document that proves your title. So when someone says they need a copy of their title, what they usually need is a copy of the recorded deed.

Your closing documents should also include a copy of the deed. If you cannot find it, your real estate attorney or the title company that handled your closing may be able to provide a duplicate.

How Deed and Title Work Together at Closing

When you buy a home, you receive both the deed and the title. They work hand in hand during the closing process, but they serve different roles.

Before closing, a title company or real estate attorney will conduct a title search. This involves reviewing public records to confirm that the seller actually owns the property and that there are no outstanding claims, liens, or encumbrances against it. The goal is to make sure the title is “clear” so the buyer is not inheriting someone else’s problems.

If the title search comes back clean, the closing can move forward. At closing, the seller signs the deed, which officially transfers the title from the seller to the buyer. The deed is then recorded with the county, and the buyer is now the legal owner.

If the title search reveals issues, those problems need to be resolved before closing can happen. This might mean paying off an old lien, correcting a name error on a previous deed, or settling a dispute with a third party who claims an interest in the property.

Title Search and Title Insurance: Protecting Your Investment

A title search is one of the most important steps in the home buying process. It digs into the property’s history to uncover any potential problems before you take ownership. A thorough title search will reveal previous owners, past liens or mortgages, easements, judgments, and any other encumbrances that could affect your ownership.

The result of that search is sometimes called an abstract of title, which is essentially the property’s legal paper trail.

Title insurance is an additional layer of protection that covers you if something slips through the cracks. There are two types. Lender’s title insurance protects the mortgage company and is typically required when you are financing the purchase. Owner’s title insurance protects you as the buyer and is optional but highly recommended.

Here is why owner’s title insurance matters. Imagine you buy a home and everything looks clean at closing. Two years later, a relative of a previous owner comes forward claiming they inherited the property. Without owner’s title insurance, you could be stuck paying legal fees and potentially losing the home. With a policy in place, the insurance company handles the defense and covers losses up to the policy amount.

I always tell my clients to seriously consider owner’s title insurance. The one-time premium you pay at closing is a small price compared to the financial disaster of an unexpected title dispute down the road.

Frequently Asked Questions

Q: What is the difference between a deed and a title?

A: A deed is a physical legal document that transfers ownership of property. A title is the legal concept representing your ownership rights. The deed is the tool that moves the title from seller to buyer.

Q: Which is more important, title or deed?

A: Neither is more important on its own. They work together. The deed transfers ownership, and the title represents your legal rights as the owner. You need both for secure property ownership.

Q: Who holds the title to my home if I have a mortgage?

A: You do. The person or people named on the recorded deed hold the title. Your mortgage lender holds a lien, which is a financial interest in the property, but you remain the legal owner.

Q: How do I get a copy of my property deed online for free?

A: Visit your county’s Register of Deeds website and search by your name or property address. Many counties offer free online viewing. Downloading or ordering a certified copy may cost a small fee.

Q: What is the difference between title, deed, and mortgage?

A: A title is your legal right of ownership. A deed is the document that transfers that ownership. A mortgage is a loan secured by the property, where the lender places a lien on the title until the loan is paid off.

Q: What is a quitclaim deed?

A: A quitclaim deed transfers whatever ownership interest the grantor has without making any guarantees about the title. It is commonly used between family members or spouses when no money is changing hands.

Q: Should I get title insurance when buying a home?

A: Most experts recommend it. Lender’s title insurance protects the mortgage company, not you. Owner’s title insurance is optional but covers you if an unknown claim or defect shows up after closing.

The Bottom Line

The difference between deed and title is one of those real estate basics that sounds simple once someone explains it, but causes real confusion when nobody does. A deed is the document. A title is the right. You need both to officially own a home, and understanding how they work together will make the entire buying or selling process less intimidating.

Whether you are looking to buy your first home or sell your house in Michigan, do not leave these details to chance. Having an experienced real estate agent in your corner who understands the legal and practical sides of closing is the difference between a smooth transaction and a stressful one.

Have questions about buying or selling a home in Michigan? I am here to help. Reach out for a free 15-minute strategy session and let us build a plan that works for your situation.

Firas Hanna | Licensed Michigan Realtor | MBA

248-703-1219 | firasrealestate.com

Disclaimer: The content on this website is provided for general informational purposes only and should not be relied upon as legal, financial, real estate, or other professional advice. While we aim to ensure the information is accurate at the time it is written, we make no guarantees regarding its accuracy, completeness, or currency. You should consult a qualified professional before making any real estate or financial decisions.