You can sell your house the same day you close on it. There is no law that says you have to wait. However, selling too soon after buying a house can cost you thousands of dollars in taxes, fees, and lost equity. Most financial and real estate professionals, myself included, recommend waiting at least two years before selling. That said, life does not always follow a neat timeline. I am Firas Hanna, a licensed Realtor in Michigan, and I have personally helped clients navigate early home sales when circumstances made it necessary. In this guide, I am going to walk you through exactly what happens when you sell a house shortly after buying it, what it could cost you, and how to make the best decision for your situation.

Can You Legally Sell a House Right After Buying It?

Yes. Once you close on a property and the deed is in your name, you are the legal owner. You can list it for sale the next day if you want to. There is no federal or Michigan state law that requires you to live in a home for any specific amount of time before selling it. If you want to understand the difference between owning the deed and holding title, take a look at our breakdown of deed vs title.

That said, certain loan programs do come with occupancy requirements. If you used an FHA loan, you agreed to use the home as your primary residence. The FHA also has anti-flipping rules that can create extra hurdles if a property is resold within 90 days of the previous sale. If you used a VA loan, there are similar primary residence expectations. Violating these terms does not mean you cannot sell, but it could complicate the process and potentially flag your loan.

The real question is not whether you can sell your house 3 months after buying it. The real question is whether it makes financial sense to do so.

What Happens Financially When You Sell a House Too Soon?

Selling a house is not free. Between agent commissions, closing costs, and potential tax hits, an early sale can eat into your proceeds fast. Here is what to watch for.

Capital Gains Tax

This is the biggest financial factor when selling a house before two years. If you sell your primary residence and make a profit, the IRS allows you to exclude up to $250,000 of that gain from your taxable income if you are single, or up to $500,000 if you are married filing jointly. But to qualify for that exclusion, you must have owned and lived in the home for at least two of the five years before the sale.

If you sell before hitting that two year mark, any profit you make is subject to capital gains tax. Sell within one year and you are looking at short-term capital gains, which are taxed at your ordinary income tax rate. That could be anywhere from 10% to 37% depending on your bracket. Sell after one year but before two and you face long-term capital gains rates of 0%, 15%, or 20%, which are lower but still significant.

There are some exceptions. If you need to sell due to a job relocation, a health condition, or certain unforeseen circumstances, you may qualify for a partial exclusion even if you have not hit the two year mark. I always recommend speaking with a CPA or tax professional before making this decision. Tax rules change, and your specific situation matters. For the official rules, you can review IRS Topic No. 701: Sale of Your Home.

Closing Costs and Agent Commissions

When you bought your home, you likely paid somewhere between 2% and 5% of the purchase price in closing costs. When you sell, you face another round of costs. Seller closing costs, agent commissions, title fees, transfer taxes, and other expenses can add up to roughly 8% to 10% of the sale price.

If you bought a home for $300,000 and sell it a year later for $310,000, that $10,000 in appreciation could easily be wiped out by the combined cost of buying and selling. This is one of the most common mistakes buyers and sellers make when they do not plan ahead.

Limited Equity

In the first few years of a mortgage, the majority of each monthly payment goes toward interest rather than principal. That means you are not building equity as fast as you might think. Unless your home has appreciated significantly or you made a large down payment, you may owe more on the mortgage than you can net from the sale after all costs are factored in.

Mortgage Prepayment Penalties

Most modern mortgages do not include prepayment penalties, and FHA loans never do. However, some conventional loans and certain specialty products still carry them. A prepayment penalty typically usually ranges from 2% to 5% of the remaining loan balance. Before you list, check your mortgage agreement or call your lender to confirm whether a penalty applies. The Consumer Financial Protection Bureau is a good resource for understanding your mortgage rights.

Is There a Penalty for Selling a House Before 1 Year?

There is no specific legal penalty for selling a house before one year. You will not get fined by the government just for selling early. However, the financial penalty for selling a house before 1 year comes in the form of short-term capital gains tax, which is the highest rate you can face on any profit from the sale.

On top of that, you will have had almost no time to build equity. Your first year of mortgage payments barely touches the principal balance. When you add up the closing costs from buying, the closing costs from selling, agent commissions, and potential moving expenses, most homeowners who sell within the first year end up losing money on the transaction even if the home itself went up in value.

If you are in a situation where you must sell within a year, talk to a local Realtor first. An experienced agent can run the numbers with you and help you understand exactly where you stand before you commit to listing. If you are not sure what to look for in an agent, here is a guide on choosing the right Realtor in Michigan.

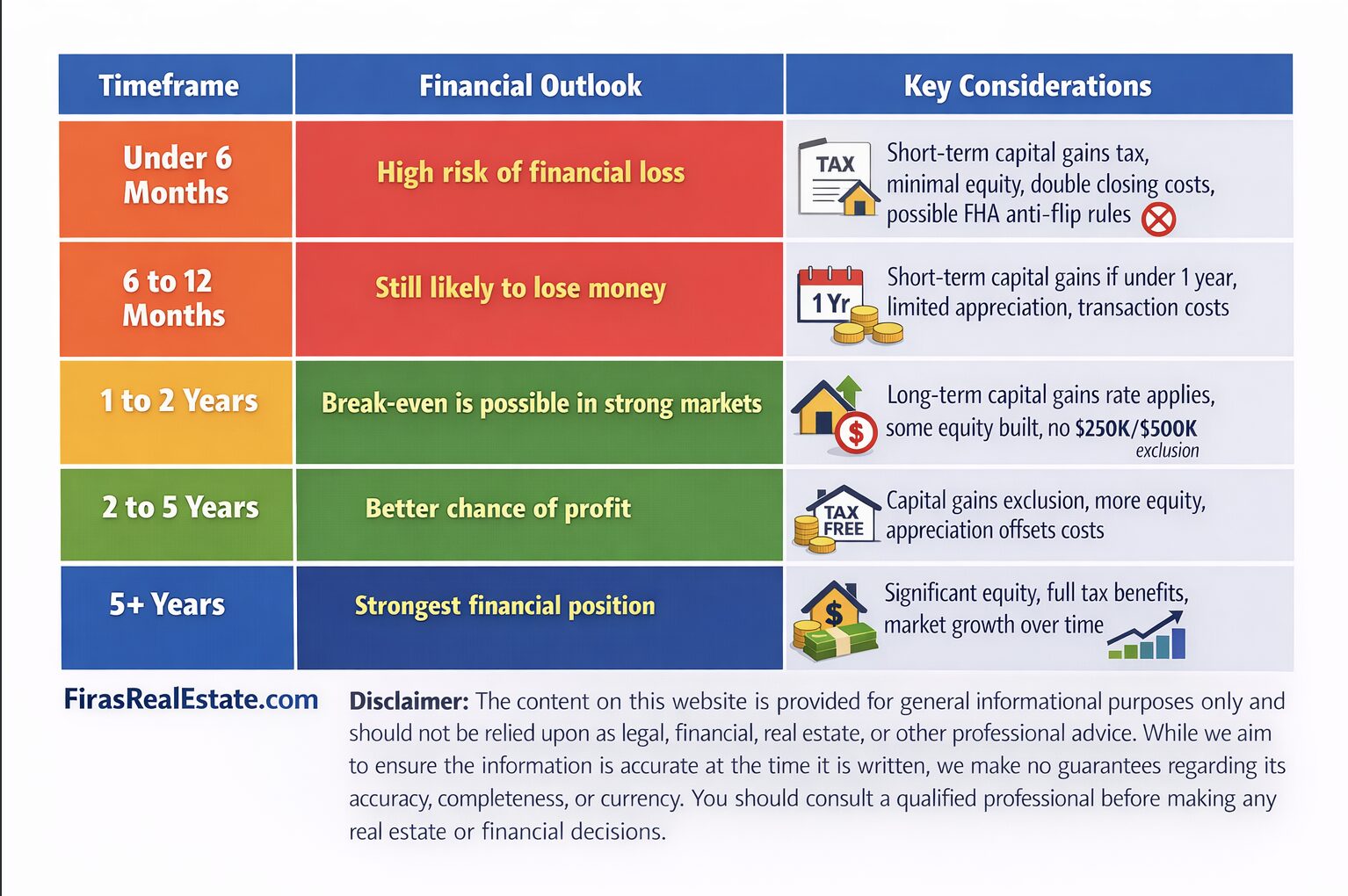

Selling Your House After Buying It: A Timeline Breakdown

Every situation is different, but here is a general overview of what to expect depending on how long you have owned your home.

For more details on exclusion rules, see IRS Publication 523: Selling Your Home.

What I Tell My Clients: A Real Example

Not long ago, one of my clients asked me, “How soon after buying a house can you sell it?” I had worked with a client who had just moved to Michigan and purchased a home. Within two years, a job opportunity came up in Texas that he could not pass up. He ended up needing to sell his Michigan home much sooner than he originally planned.

We sat down and looked at everything together. We reviewed his mortgage payoff amount, estimated what the home would sell for in the current market, calculated the closing costs and commissions, and talked through the tax implications with his CPA. By approaching it step by step instead of rushing into a listing, we were able to price the home correctly, avoid unnecessary costs, and make the transition as smooth as possible.

That experience is exactly why I tell every client the same thing. Sometimes you have to do what you have to do. Life does not wait for the perfect two year mark. But if you take the process step by step and work with the right professionals, you can minimize the financial impact and move forward with confidence.

When Selling Your House Early Actually Makes Sense

While waiting is usually the smarter financial move, there are situations where selling early is the right call. Here are a few I see regularly in my work across Metro Detroit.

A job relocation that requires you to move out of state or to a different part of the country is one of the most common reasons. If the new opportunity significantly increases your income, the cost of an early sale may be worth it in the long run.

A major life change like a divorce, a growing family, or a health situation that requires a different living arrangement can also make an early sale necessary. In these cases, holding onto a home that no longer fits your life can cost you more in stress and ongoing expenses than selling at a slight loss.

If you purchased the home significantly below market value, perhaps through a foreclosure, short sale, or estate sale, you may have built in equity from day one. In that scenario, selling early could still result in a profit even after accounting for all the costs. If you are curious about whether a fixer-upper or turnkey home is the better investment strategy, we break that down in a separate guide.

Finally, if you discover major defects or neighborhood issues after moving in that were not disclosed during the purchase, it may be better to cut your losses early rather than deal with ongoing problems.

Alternatives to Selling Your Home Early

If you are on the fence about whether to sell, consider a few alternatives before making a final decision.

Renting out your home is one option. If you need to relocate but the numbers do not work for a sale, becoming a landlord can help you cover the mortgage while you build equity and wait for a better time to sell. Keep in mind that being a landlord comes with its own responsibilities and costs, so run the numbers carefully.

Refinancing your mortgage could also help if the issue is monthly affordability rather than needing to move. A lower interest rate or extended term could reduce your payments enough to make staying worthwhile.

If you are dealing with financial hardship, talk to your lender before assuming a sale is your only option. Many lenders offer forbearance programs, loan modifications, or other solutions that could give you time to recover without losing your home. Whether you are staying or going, knowing the essential questions Michigan home buyers need to ask can help you make better decisions on your next move too.

How to Sell Your House Quickly After Buying It Without Losing Your Shirt

If you have decided that selling is the right move, here is how to approach it the right way.

First, hire a local Realtor like me, who understands your market. Someone who knows your specific city and neighborhood can price your home accurately from the start. Overpricing an early sale is one of the biggest mistakes I see, and it usually leads to the home sitting on the market, which raises even more red flags for buyers.

Second, talk to a CPA or tax professional before listing. Understanding your potential tax liability upfront allows you to factor that into your pricing and negotiation strategy.

Third, be transparent in your listing about why you are selling. Buyers may wonder why a home is back on the market so quickly. A simple explanation like “seller relocating for work” eliminates doubt and keeps buyers focused on the property itself.

Fourth, do not rush the process. I know that sounds counterintuitive when you are trying to sell quickly, but rushing leads to mistakes. Skipping a home inspection, underpricing the home, or accepting a bad offer just to get it done can cost you more than waiting a few extra weeks for the right deal. If you want a deeper look at how to approach a sale with confidence, check out our guide on how to sell my house with confidence in Michigan.

Final Thoughts on How Soon You Can Sell a House After Buying It

How soon after buying a house can you sell it? Legally, right away. Financially, the smart move is usually to wait at least two years so you can take advantage of the capital gains tax exclusion and give yourself time to build equity. But I also know that life does not always cooperate with financial timelines.

If you are in a situation where you need to sell sooner than planned, the most important thing you can do is surround yourself with the right team. A knowledgeable Realtor, a good CPA, and a clear understanding of your numbers will help you make the best decision for your circumstances.

I have helped clients across Michigan navigate exactly this kind of situation, and I would be happy to help you figure out your next step. Whether you are exploring the best places to live in Michigan for your next home or just want to understand your options on selling your current one, reach out for a free 15-minute strategy session and let us put a plan together.

Ready to talk? Call or text Firas Hanna at 248-703-1219 to book your free strategy session.

Firas Hanna | Licensed Realtor | MBA | 248-703-1219 | firasrealestate.com

Disclaimer: The content on this website is provided for general informational purposes only and should not be relied upon as legal, financial, real estate, or other professional advice. While we aim to ensure the information is accurate at the time it is written, we make no guarantees regarding its accuracy, completeness, or currency. You should consult a qualified professional before making any real estate or financial decisions.